or Call 866.679.9410

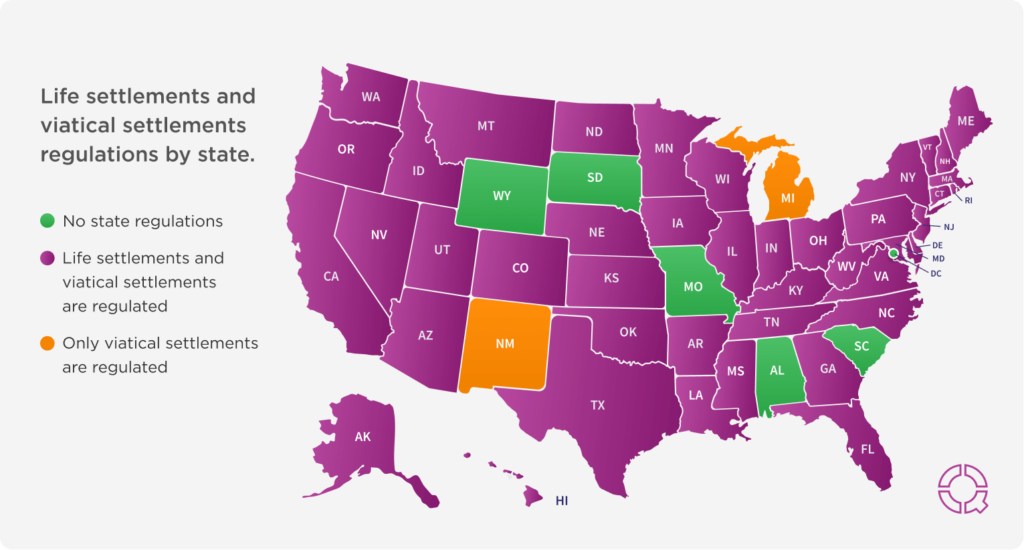

Life and viatical settlements are regulated at the state level, meaning your state’s insurance or financial services department sets the rules for these transactions. Learn more.